The Tax Surprise: Why Unclaimed Property Recovery Can Create Unexpected IRS Obligations

When Robert recovered $8,400 from his late father’s forgotten bank account, he was thrilled until his CPA explained he owed nearly $2,000 in federal taxes, plus possible state tax obligations. Stories like Robert’s are increasingly common as Americans discover billions of dollars in unclaimed property through official state programs.

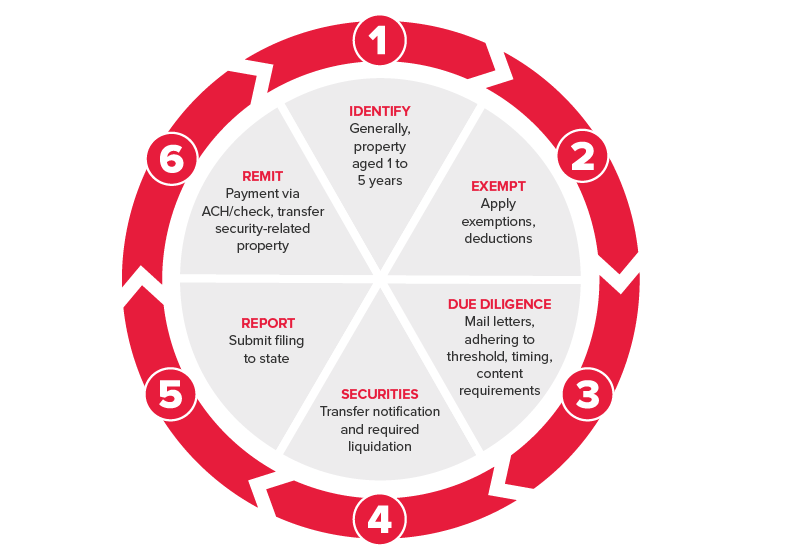

Figure. Six-step unclaimed property compliance cycle: identify, exempt, due diligence, securities, report, and remit

What many don’t realise is that recovered unclaimed property is often taxable income under federal law. From forgotten bank accounts to uncashed paychecks, IRS rules require taxpayers to report recoveries, sometimes creating immediate obligations.

This article describes how federal tax applies to unclaimed property, including how income is recognised and how that income is treated as part of an estate, the impact on the business, and tax planning. Taxpayers can evade fines, minimise tax liability, and comply adequately in reclaiming their long lost money.

IRS Income Recognition: When Unclaimed Property Becomes Taxable

The Internal Revenue Code (IRC) is very broad. Section 61 provides gross income which entails all income from whichever source which including the majority of the unclaimed property recovered.

Key principles:

- Timing matters: Income is recognised in the year property is recovered, not when originally earned.

- Cash vs. property: Monetary recoveries are reported at face value, while tangible items (like stock certificates) are taxed based on fair market value.

- Constructive receipt: Income is taxable once made available, even if not withdrawn.

- Claim of right doctrine: Once taxpayers have full rights to recovered funds, the IRS treats it as income, even if earned years earlier.

- Original source relevance: Ordinary income is taxed on the wages, but the investment assets can attract capital gain rules.

The framework would make sure that the IRS would collect taxes on economic benefits when they are received rather than when they are initially unclaimed.

Different Types of Unclaimed Property and Their Tax Treatment

Not all unclaimed property is treated the same under tax law:

- Bank accounts: Ordinary income is generally the accumulated interest but not the principal.

- Death benefits of life insurance: Death benefits of life insurance are usually tax-free except that accumulated interest is taxable. Refund in property insurance can be subject to taxation.

- Recoveries associated with employment: Wages, bonuses and commissions are subject to taxation as ordinary income.

- Investments: Dividends, interest or capital gains distributions are taxed as normal investment income.

- Estate recoveries: The inherited property is usually eligible for a step-up in basis, and decedent income in respect of a decedent (IRD) is taxable.

- Real estate proceeds: The proceeds of sales of property recovered can result in capital gains.

- Court settlements: Tax treatment is based on whether or not payments are in the form of wages, damages, or other income.

- Pensions and retirement accounts: Retirement distributions made back to a 401(k) or IRA are usually taxable.

To ensure that they utilise the right IRS regulations, taxpayers should pay significant attention to classifying recoveries. Underreporting fines may be caused by misclassification.

Tax Planning Strategies and IRS Compliance Requirements

The tax burden of the recovery of unclaimed property should be planned to be managed.

- Estimated payments: Estimated taxes can include significant recoveries with the need to pay one quarter to avoid the penalties of underpayment.

- Form 1040 reporting: Recoveries of various types (interest, wages, dividends) need to be put on the appropriate line items.

- Documentation: retain state recovery letters and valuation records to be audited by IRS.

- Amended returns: If recoveries relate to prior years’ income, taxpayers may need to adjust old filings.

- Withholding adjustments: Employees may make higher withholding in current year so that they can counteract recovery income.

- Harvesting tax losses: This entails capital losses used by investors to offset the taxable gains.

- Charitable contributions or retirement: Elevated contributions can be matched with tax deductions.

That is why it is so complicated to define how to treat taxation within each category, and some resort to such tools as Claim Notify to be clear about what to claim. Through preestablished knowledge of the IRS rules, the taxpayers will be able to reclaim property before being caught in the crossfire of taxation.

Estate and Inheritance Tax Considerations

Unclaimed property often surfaces in estates, creating special tax challenges.

- Step-up in basis: Fair market value basis is usually applied to inherited assets, so that the capital gain is minimised on sale.

- Estate inclusion: the recovered property can add to the taxable estate and this can change the estate tax levels.

- IRD (Income in Respect of a Decedent): Retirement accounts or unpaid wages or annuities continue to be taxed to the heirs.

- Beneficiary requirement: An heir might be required to report his or her portion of taxable income.

- Trusts and estates: In the case of the recovery of unclaimed assets by estates, the income can be reported at the entity level or paid to the beneficiaries.

- Charitable planning: Heirs may disclaim recovered property or donate it to reduce estate tax liability.

In the case of families, unclaimed property may make the settlement of estates that are already challenging. The active coordination with the attorneys of the estate and tax professionals is also the assurance of compliance and the minimisation of surprises.

Business and Self-Employment Tax Implications

Companies and self-employed people have special regulations for reclaiming unclaimed property.

- Business vs. personal classification: When the money is associated with the activities of the company, it should be included as the business income.

- Self-employment tax: Freelance or gig income recovered is taxable both in terms of income and self-employment tax.

- Recapture of depreciation: Recapture income can be generated with the recovery of depreciated assets under the IRC rules.

- Partnerships and S-Corps: Unclaimed distributions flow through to partners or shareholders.

- NOL utilisation: Businesses may offset taxable recoveries with net operating losses.

- 199A deduction: Some recoveries can receive the 20 percent pass-through deduction.

The inability to provide the right classification can result in an IRS audit. In the case of businesses, it is important that correct reporting and good recordkeeping are taken when there are cases of unclaimed properties which are related to commercial activity.

Proactive Tax Planning for Unclaimed Property Success

The unclaimed property recovery should be a win-win situation monetarily, without tax planning, however, it tends to become a liability. Most recoveries are considered taxable income by the IRS, generating reporting and payment and planning burdens.

Strategies that might be taken into account prior to filing a claim by taxpayers are to think about the possible liabilities, liaise with the CPAs, and consider the strategies that might be taken, which may be withholding adjustments, charitable giving, or retirement contributions. Business entities must report correctly to prevent punishment.

The tools such as ClaimNotify assist Americans in recognising recoveries and plan what to do with taxes beforehand. Through proper planning, the taxpayers can convert the unwanted property into a planned financial gain that can be to the best of their recovered property as well as their claimed property as a means of ensuring that they comply with the law and receive maximum benefit of the property they have claimed.